State-owned banking giant Vietcombank has announced its business performance for the first half of the year, in which pre-tax profit hit a record $485.2 million, representing 54 per cent of the annual target and nearly equal to the result for 2017 as a whole. Its profit figure is also expected to be the highest in the country’s banking system for the first half. A number of other Vietnamese banks also disclosed positive business performance in the first half, with new records being set.

Outstanding performance

Vietcombank’s impressive results were attributed to its success in pursuing strategies to strongly shift from the wholesale to retail banking segment, boost capital for investment activities, and increase the proportion of revenue from services over the last three years. Shareholders are now looking forward to the remainder of 2019, as the annual target of around $880.7 million in pre-tax profit is well within reach.

Asia Commercial Bank (ACB), which is among ten banks earmarked for adopting Basel II standards, and HDBank (HDB) also reported outstanding results. ACB’s pre-tax profit was $155.5 million, or half of the annual target. It has asked the State Bank of Vietnam (SBV) to raise its credit growth limit from 13 to 17 per cent for 2019, which is testament to its expanding credit activities. HDBank put half-year earnings at more than $95 million, with a 1.7 per cent return on assets (ROA) and a 20 per cent return on equity (ROE).

Other lenders such as Vietnam International Bank (VIB), TPBank (TPB), and Sacombank (SCB) posted solid results, placing them in the “trillion VND” group. VIB saw its pre-tax profit increase 58 per cent year-on-year, ending June at $78.4 million. Total revenue was $157.7 million, up 36 per cent year-on-year. Income excluding interest rose 68 per cent and accounted for 20 per cent of the total. The bank prides itself on being a leader in bancassurance and credit card growth.

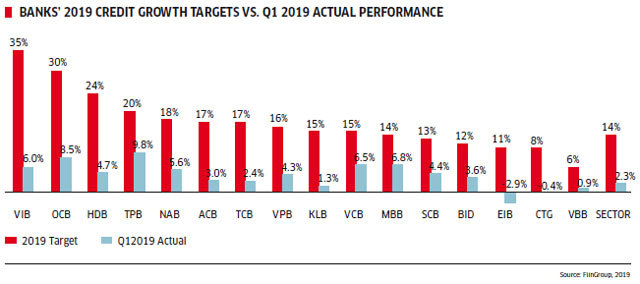

Credit growth in the banking sector overall in the first half was lower year-on-year, at 7.33 per cent against 7.82 per cent in the first half of 2018. Ms. Nguyen Thi Que Anh, Analyst at MB Securities (MBS), said this growth - the lowest in four years - is necessary for Vietnamese banks to focus on credit quality and cut non-performing loans. Lending structures also switched to a retail-oriented direction, with a primary focus on the manufacturing sector.

Lower earnings growth is expected in the first half, due to an absence of one-off income sources being recorded. But core income growth remained at its previous rate, with the main slice coming from fee and service income. “We have seen a leap in digital transformation in the industry, which boosted settlement revenue by more than 20 per cent year-on-year,” she said. “Bancassurance’s high growth, of more than 40 per cent year-on-year, continued adding value.”

The positive results posted by local banks originate from strong credit growth and the recovery or resolution of bad debts, according to Mr. Le Xuan Dong, Director of Market Research Services at FiinGroup (formerly StoxPlus). “While the targeted credit growth remains at 14 per cent overall, the SBV maintains that only banks that have met capital adequacy ratios (CARs) may be allowed to enjoy a higher ceiling,” he explained. “Those that managed to meet the Basel II requirements have therefore been reporting strong performance, with net profits exceeding expectations. With half a year left and new credit growth ceilings, these banks could expect even higher profit growth by the end of 2019.”

Lower-tier players Sacombank and Nam A Bank (NAB) also reported strong performance in the first half. Sacombank, which holds the highest NPLs in the sector, has seen recoveries in its bad debt positions, especially in real estate. As for NAB, positive credit growth of around 8 per cent in the first half boosted its earnings. The second half performance of these banks, however, remains difficult to gauge given the constraints on their credit growth and asset quality.

|

New drivers

Eight of a total of 17 listed banks have met or are getting close to meeting Basel II requirements. These banks can expect a bright outlook for the second half as credit growth limits are lifted, allowing them to both expand their retail loan portfolio and their fee and commission revenues.

Meanwhile, Mr. Dong noted, for large, listed State-owned commercial banks (SOCBs) such as Vietcombank and BIDV, the growth story will not be as positive given their CAR constraints. Others are either small (Bac A Bank and National Citizen Bank) or have their own problems to resolve (such as high NPLs at STB or corporate governance issues at Eximbank (EIB)), resulting in conservative loan portfolio expansion which will limit how much they can grow. If these banks have overreached in the first half, they are likely to see a slowdown in the second half.

Given the constraints on credit growth in the second half, banks could look to other factors to boost profitability. In terms of net interest income, reducing the cost of funding is a concern for retail-oriented banks. For those such as Techcombank (TCB) and Military Bank (MB), increasing current account/savings account (CASA) is a key driver in increasing low-cost funding.

Retail banking and non-interest income are actually advantages for banks. The total contribution of retail lending to total lending was approximately 38 per cent in 2018 and increasing, which enhances net income margins (NIMs) remarkably thanks to banks having a higher bargaining power. “We think that retail lending, particularly lending for consumption and housing, has been a good direction to take over recent months thanks to better margins and a growing mass-affluent and affluent class, with a compound annual growth rate (CAGR) of 11 per cent year-on-year expected between 2018 and 2030,” Ms. Que Anh said.

The expansion towards retail banking, which includes not only retail lending for housing and credit cards but also promotes card and payment services and bancassurance, continues to bring in profits to banks. The trend of boosting bancassurance partnerships has also contributed significantly to net income. For example, at VIB, bancassurance revenues account for 70 per cent of income from fees and commissions, and in turn contributed 32.6 per cent of operating income in the first half of this year.

Furthermore, the recovery of written-off bad debts is still going strong. NPLs in Vietnam’s financial system have seen a downward trend. Since Resolution No. 42 was issued in 2017, banks have been much more active in bad debt settlement and have been capitalizing on the warm real estate sector to resolve their bad property assets. In the second half of this year, the recovery of written-off debts may continue to play a role in some banks’ profit growth.

After one-off exclusive income was recorded in 2018, considering the positive economic signs, spiking GDP per capita, and low penetration of bancassurance in Vietnam, MBS estimates that bancassurance will continue to expand by an average of more than 40 per cent year-on-year at private commercial banks such as MBB, TCB, and VIB.

|

Overcoming boundaries

In the time to come, local banks will be forced to maximize profits on their lending assets by actively choosing higher-yield borrowers with better creditability to minimize provision expenses, according to Ms. Que Anh. Retail lending to individuals will minimize concentration risks to dominant customers while lending to small and medium-sized enterprises (SMEs) and corporates with potential earnings growth will diversify NPL risk.

Moreover, in combination with traditional lending to those segments, banks can also exploit cross-selling other non-credit products. For instance, life insurance attached to lending, settlement fees from banking transactions, and other wealth management fees would enhance non-interest income (NII). MBS believes that digital banking has been transforming the income structure at Vietnamese banks and making them less dependent on margin earnings and moving towards transactional banking.

Increasing core capital is needed for banks to comply with Basel II and have opportunities for credit expansion. SOCBs will face pressure in the immediate future to complete private placements to foreign investors, while private banks will execute share dividend plans to strengthen charter capital.

Mr. Dong from FiinGroup warned that banks that can’t meet prudential requirements will face severe challenges in the second half of the year as a result of credit growth ceilings. If local banks can’t grow their outstanding credit, they will face competition from their peers and lose customers as well as the associated income. These banks also face increasing NPLs due to loans made during previous growth periods turning bad.

Banks are actively seeking other sources of income, such as fees and commissions from services. Partnerships and/or integration into existing ecosystems are key competitive advantages that banks could gain to boost payment volumes and fee income.

Another point to consider is cost efficiency. The cost-to-income ratios at 26 selected banks in Vietnam studied by FiinGroup fell from 45 per cent in 2015 to 41 per cent in the first quarter of this year, revealing improvements in cost management. Investments in digitalization will begin to bear fruit as banks can leverage their platforms to offer more retail banking services, expand their customer base, or automate their internal processing without hiring more staff or opening new branches. VN Economic Times

Hung Cao

Bancassurance becomes main service earner for banks

Instead of the modest contribution made previously, the insurance business segment, or bancassurance (banks co-operate with insurers to sell insurance products), has now become the main source of income from service activities for many banks.

VN banks thrive with satisfactory profits, despite low credit growth

Many commercial banks have reported profits of trillions of dong in the first half of the year.