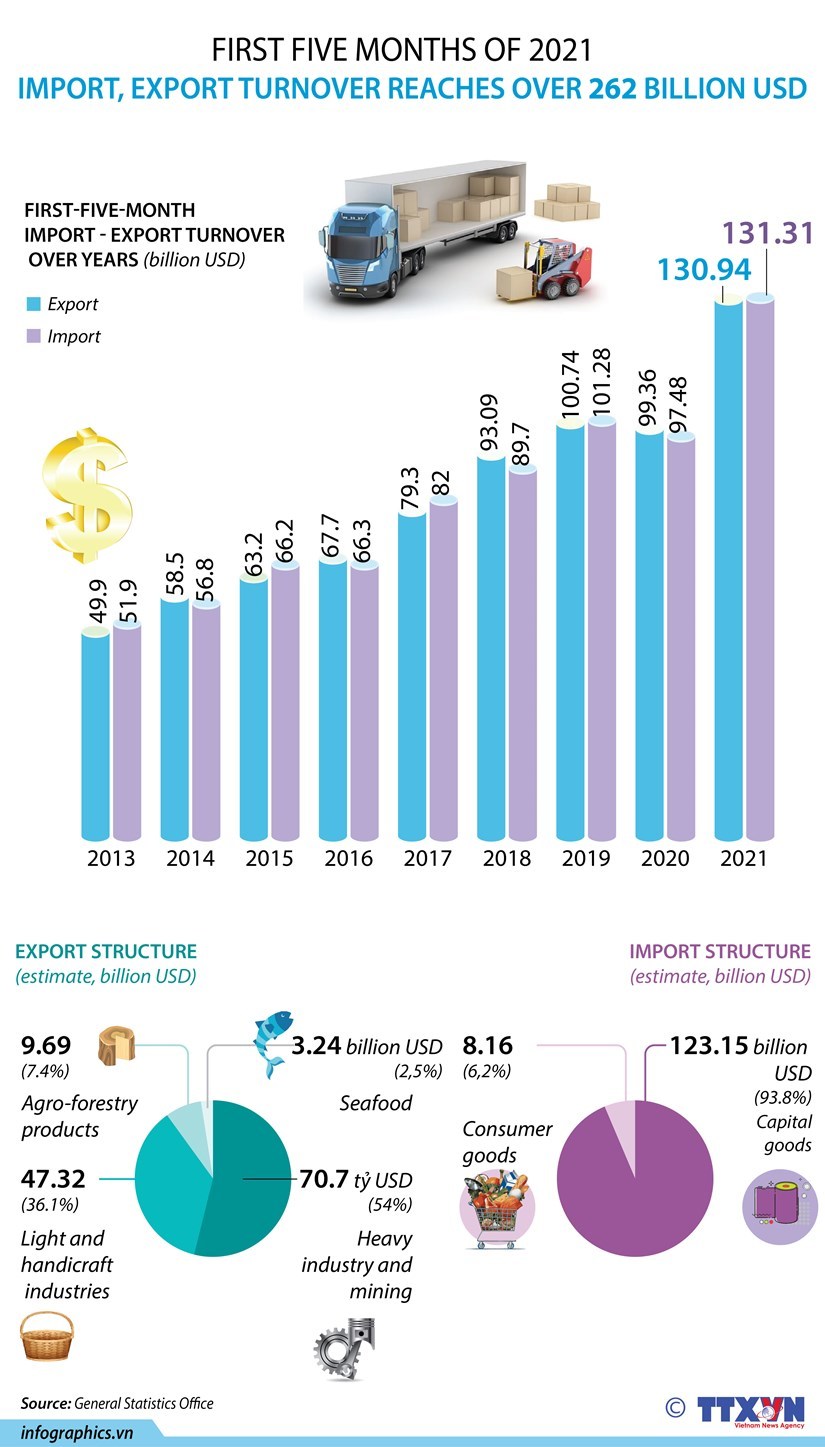

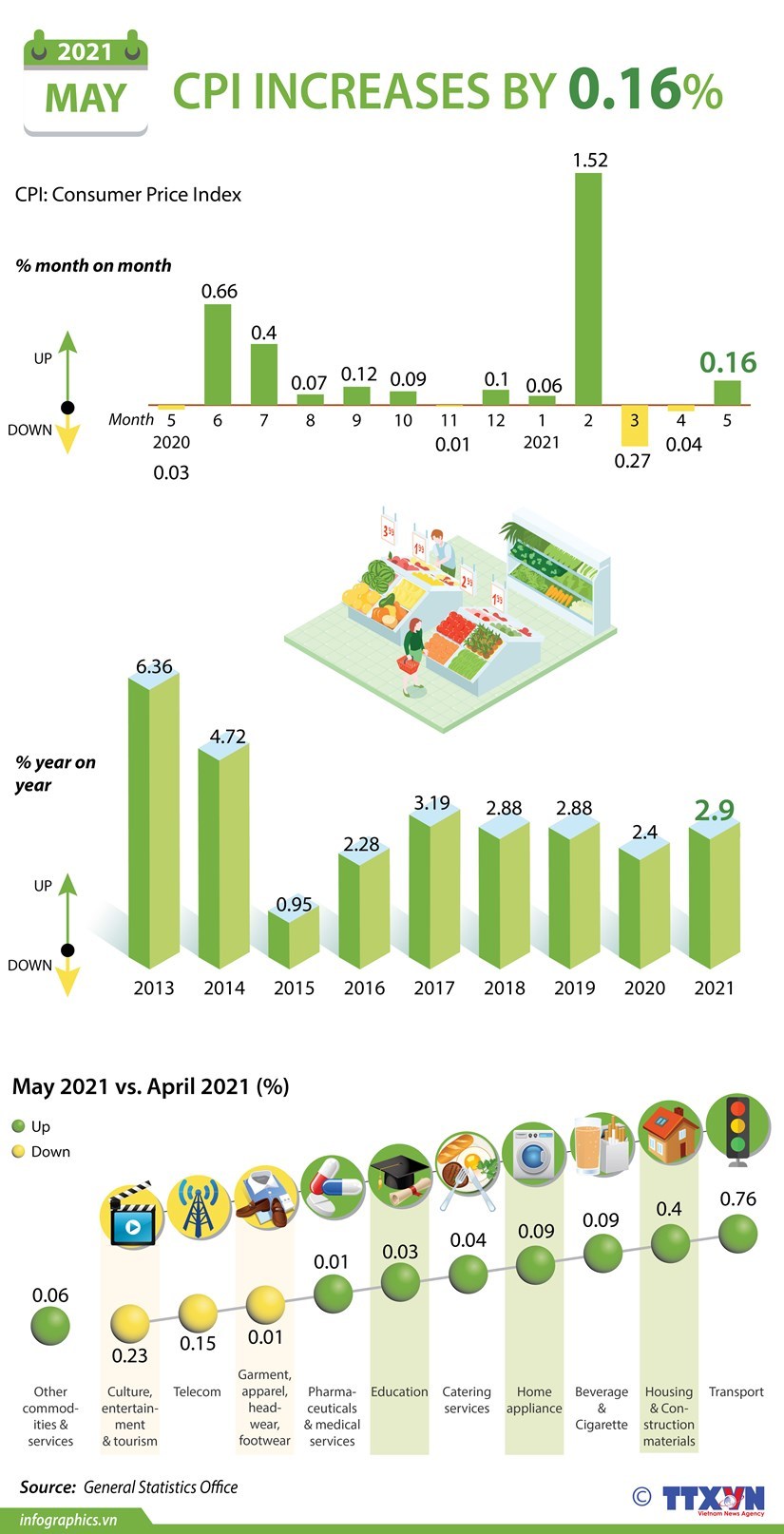

|

|

|

E-commerce has not only become an effective tool to help enterprises overcome obstacles posed by the pandemic but is also expected to act as a key to clearing the way for Vietnamese goods to make further inroads into the global market.

E-commerce in Vietnam is being expanded with many models and players, and supply chains are gradually being modernised with the assistance of digitisation and information technology.

With a young population and high smartphone ownership, Vietnam has seen rapid growth in e-commerce with 35 million users, creating revenue of US$11.8 billion in 2020, accounting for 5.5% of total retail sales and consumer services, compared to 4.9% a year earlier.

A report by Google, Temasek and Brain & Company on e-commerce in Southeast Asia has projected growth of 29% for Vietnam’s e-commerce market during the 2015-2025 period. The size of e-commerce in Vietnam is forecast to reach US$43 billion in 2025, ranking third in ASEAN.

Amid the impacts of Covid-19, the e-commerce market is becoming more dynamic, and the creation of new distribution channels on digital platforms is helping Vietnamese enterprises overcome difficulties and change consumers’ shopping habits - from physical to online stores.

Cross-border e-commerce is also an effective means for Vietnamese enterprises to participate in the global supply chain, helping reduce risk when traditional supply chains are disrupted.

According to Director of the Vietnam E-Commerce and Digital Economy Agency (IDEA) Dang Hoang Hai, despite recognising the benefits of expanding further into the global market through e-commerce, many Vietnamese sellers remain hesitant as they have yet to acquaint themselves with the procedures related to export through e-commerce and display a lack of knowledge in the area.

IDEA has rolled out various programmes to help Vietnamese enterprises adopt this method. Most recently, IDEA collaborated with Amazon Global Selling to provide knowledge on cross-border e-commerce for Vietnamese sellers, support the setup and operation of stores on Amazon and improve competitiveness so as to expand their scope of business to more countries.

Director of Amazon Global Selling in Vietnam Gijae Seong said Vietnam is one of the most dynamic emerging economies in the world and has demonstrated its firm position amid the Covid-19 pandemic. Amazon wishes to make more contributions to the development of cross-border e-commerce in Vietnam and promote Vietnamese enterprises to reach further into the global market, said Seong.

The Amazon official added that the retailer is actively realising that by expanding cooperation with organisations in Vietnam, training small and medium-sized enterprises in cross-border e-commerce skills, fostering changes to the future of Vietnam’s export and digital economy.

The breakneck growth of e-commerce recently has made Vietnam one of the markets with the greatest potential in ASEAN. But besides benefits such as helping enterprises widen their markets, cut costs, increase profits and fast payment, there are several drawbacks of trading online.

Fake and smuggled goods and goods in violation of intellectual property rights are quite commonplace on many digital shopping sites. Social media networks are also emerging as popular e-commerce platforms, but are not properly regulated.

IDEA is proposing a new decree to regulate e-commerce activities, including mandatory requirements on publicising product information in order to make it transparent to consumers, aiding in the prevention of trade fraud. The new decree will also change the regulations on the presence of sellers and foreign organisations engaged in e-commerce in Vietnam.

IDEA is also building an e-commerce credit platform as a tool to evaluate those doing business in the online space and credit ratings will be widely announced to consumers.

Tan Yen fresh lychees hit shelves in Japan

Lychees grown in Tan Yen district, the northern province of Bac Giang have made their way to stores in Japan this year.

The first shipment of early-ripening lychee was sent to the East Asian country at a ceremony at the end of May. From May 24-26, around 20 tonnes were exported to Japan.

This is the second year that the local staple has been exported to this fastidious market, and the achievement is more special as it is attained during the COVID-19 pandemic.

Chairman of the Bac Giang provincial People’s Committee Le Anh Duong said local authorities have taken measures to ensure the quality, food safety and hygiene of the fruit.

Speaking at the ceremony, Phan The Tuan, vice chairman of the provincial People’s Committee said in the context of complicated changes caused by the COVID-19 pandemic, Bac Giang province has built strong lychee growing areas, especially in Tan Yen and Luc Ngan districts.

The province has prepared necessary conditions to ensure absolute safety in terms of health, security and order for businesses, traders, and drivers entering Bac Giang to purchase and consume lychee. The first shipment of lychees exported to Japan, a large market with very high quality standards, has shown the locality’s determination, seriousness and responsibility in the process of producing and consuming lychee, he added.

The authorities also actively worked with the Japanese Embassy in Vietnam to receive a Geographical Indication (GI) certificate for lychees grown in Luc Ngan district, making it the first Vietnamese product to obtain such certification from Japan.

Since the pandemic has seen complicated developments, particularly as Bac Giang is now one of the country’s hotspots, the provincial authorities have well prepared for lychees consumption this year.

Nguyen Viet Toan, Chairman of Tan Yen District People's Committee, said: “In 2021, in the context of the COVID-19, the district will focus on protecting lychee areas from the pandemic such as persuading local residents to refrain from travelling out of the areas, setting up checkpoints to control people and vehicles entering the concentrated lychee area, and keeping close health monitoring of local farmers as well as seasonal labourers working in fruit harvesting and transport.”

This year, Bac Giang province has around 28,100 ha of lychees with an estimated output of more than 180,000 tonnes, an increase of 15,000 tonnes year-on-year. This includes 45,000 tonnes of early-ripening lychee harvested on an estimated area of 6,050 ha along with 135,000 tonnes of lychee from the main crop on an area of 22,050 ha.

“The Tan Yen early-ripening lychee has the best quality so far, ensuring food hygiene and safety and not affected by COVID-19,” he added.

The district cultivates lychee in an area of 1,329 hectares, 1,200 hectares of which are set aside for early-ripening lychee.

Many traders have come to survey and sign contract to purchase early-ripening lychees, he said, stressing each kilogramme is sold at 25,000 - 30,000 VND (1.09 – 1.3 USD), particularly the price is 55,000 VND per kilogramme for the Japanese market, and the prices are expected to increase in the coming time.

Last year, Bac Giang shipped 200 tonnes of thieu lychee to Japan.

A year after Japan first opened its market to Vietnamese lychees, the export and consumption of the fruit have been going smoothly despite COVID-19, Vietnam’s trade office in the Northeast Asian country said.

Vietnam began negotiating lychee exports to Japan in 2014. After five years, on December 15, 2019, Japan’s Ministry of Agriculture, Forestry and Fisheries announced that Japan had officially opened its market to Vietnamese lychees but also requested that the fruit undergo a strict plant quarantine process prior to export.

In early June 2020, an agricultural expert from Japan was sent to Vietnam to monitor fruit packaging and sterilisation, completing the final step required by Japan for lychees to be shipped to the market.

Thieu lychees have been exported to 30 countries such as China and the EU, Russia, the US and Canada.

Lychee is the fourth kind of fruit from Vietnam that has successfully made inroad into the Japanese market, following dragon fruit, mango and banana./.

|

|

|

Consortium led by Alibaba completes the injection of $400 million into Masan

Masan Group Corporation (HSX: MSN) today announced the completion of a private issuance of 5.5 per cent stake in The CrownX Corporation to a consortium led by Alibaba Group and Baring Private Equity Asia for a total cash consideration of $400 million.

The CrownX is Masan’s integrated consumer retail arm that consolidates its interests in Masan Consumer Holdings and VinCommerce. The transaction implies a pre-money valuation of $6.9 billion for 100 per cent of its equity, an equivalent of $93.5 per share. Masan now owns 80.2 per cent of the company. The signing of this transaction was first announced on May 18, 2021.

As part of Alibaba’s investment, The CrownX will now partner with Lazada to build the company’s digital presence and capabilities and accelerate the offline to online (O2O) market in Vietnam. This strategic partnership will accelerate the transformation of The CrownX into a one-stop shop to serve consumers’ everyday needs, whether offline or online, through its new “Point of Life” stragety.

"Our immediate priority is to modernise Vietnam’s grocery market and develop an unparalleled consumer proposition from assortment to shopping experience,” said Danny Le, CEO of Masan Group. “I strongly believe that this partnership will reduce our learning curve and enable us to reach our endgame more efficiently and effectively”.

At present, the VinMart chain is being renamed to WinMart with some stores already bearing the new brand. Masan Group also scooped up 20 per cent in Phuc Long Heritage, the operator of one of the leading tea and coffee chains in Vietnam. The two sides will jointly develop Phuc Long Kiosks through a network of more than 2,200 VinMart+ stores nationwide to bring fresh and delicious tea and coffee drinks to 100 million Vietnamese consumers.

New hope for first velodrome project in Vietnam

South Korean and Japanese investors are hoping to push up the process of the $200 million velodrome and international standard stadium that has been delayed since 2015.

The proposal for the approval of the 1/2,000 zoning plan for Rach Chiec National Sports Complex in An Phu ward, Thu Duc city on May 31 from Ho Chi Minh City Department of Planning and Architecture would be vital to saving this project, according to KP Singh, CEO of Vietnam Sports Platform (VSP), the investor of this project.

“Right after the 1/2,000 plan is approved, we will have the 1/500 plan approved and the project will be pushed forward. VPS is now also ready to contribute recommendations for the 1/500 plan of the velodrome. We are committed on processing this project even though it was delayed for years,” Singh told VIR.

VSP's velodrome and an international-standard stadium are the first projects of this type in Vietnam

Formed in November 2015, the $200 million project is invested by VSP, a joint venture between Japan Photo Promotion Co., Ltd. (30 per cent) and Korea Sports Promotion Organisation (70 per cent).

It is known that VSP is the only investor so far that has proposed a project at the Rach Chiec National Sports complex. Therefore, when officially approved, this project will be an essential factor in attracting other investors to participate in developing the complex.

After long consideration, in 2015, Ho Chi Minh City People’s Committee issued a document to permit VSP in principle to build the velodrome inside Rach Chiec National Sports Complex. The Committee had also assigned local authorities to conduct land clearance and compensation and procedures for this project.

In 2016, VSP was even ordered by the committee to push up its process for preparation to conduct this project. In March 2017, the Ho Chi Minh City Department of Planning and Architecture approved the project planning parameters.

However, soon after, Ho Chi Minh City Department of Planning and Investment (DPI) informed VSP that the selection of investors for this project must be chosen again via an open international bidding process. VSP, once more, had to submit dossiers for the bidding again.

Through the appraisal process, in 2018, the DPI submitted a report to Ho Chi Minh City People's Committee, confirming that VSP is eligible to participate in the bidding based on its technical and financial capacity. Some other contractors did not meet the set criteria and had to withdraw from the bidding process.

“VSP was confirmed to qualify to participate in the bidding based on its technical and financial capabilities in 2018. Since then, however, there is no significant progress in the approval process. We do hope that when the 1/2,000 planning of the Rach Chiec complex is approved, we will receive the official approval from the city's committee,” he said.

According to the plan, the velodrome is designed to accommodate over 6,000 seats and will be the first enclosed air-conditioned stadium on such a large scale in Vietnam. Various other Olympic standard sports such as boxing, wrestling, cue sports, fencing, judo, badminton, table tennis, and taekwondo can be conducted in this project.

The project will generate more than 1,000 jobs, promoting children and youth sports, medical facilities, public health facilities, concerts and cultural events, art gallery, public library, and sponsorships to build sports facilities at local schools.

Meanwhile, the Rach Chiec National Sports complex is expected to serve up to 100,000 people including athletes, spectators, staff, and other related subjects.

With the total investment capital of VND15 trillion ($652.17 million), this project will have 12 key components including a 50,000-seat stadium, a velodrome with motor racing and outdoor football field, a football academy, and many others.

According to Ho Chi Minh City DPI, the complex will be invested VND34 trillion ($1.5 billion), of this around VND8 trillion ($347.83 million) will be reserved for land clearance and compensation and infrastructure development.

Quang Tri proposes to develop $335 million Cam Lo-Lao Bao Expressway

Quang Tri People’s Committee proposed the prime minister to develop Cam Lo-Lao Bao Expressway in the 2026-2030 period.

The province seeks the prime minister’s approval to add Cam Lo-Lao Bao Expressway to the planning on highway construction for the 2021-2025 period with a vision to 2030.

It is expected that the expressway will have a length of 70km, a 4-lane highway standard, a 17m-wide roadbed, invested under the public-private partnership (PPP) method. The total investment capital is estimated at VND7.7 trillion($334.8 million), with the central budget contributing 28.31 per cent with a payback period of 19 years.

Quang Tri is located at the beginning of the East-West Economic Corridor connecting Vietnam with Myanmar, Thailand, Laos, and Cambodia. At present, National Highway No.9 is considered one of the important bridges linking Cam Lo with Lao Bao International Border Gate.

The problem is that vehicle traffic on Highway No.9 is increasing, including container trucks transporting goods to Laos and vice versa, causing overload, traffic jams, road hazards and endanger commercial activities. This necessitates the development of Cam Lo-Lao Bao Expressway.

Completing roadway infrastructure is a key target in highway planning in 2021-2025 with a vision to 2030.

Notably, by 2030, the country will focus on developing expressways, including the Eastern Cluster of the North-South Expressway, expressways connecting Hanoi and Ho Chi Minh City, and expressways in the Northwest Region, the Central Highlands, and the Mekong Delta Region.

Until 2025, priority expressway projects connect to the North-South Expressway (VND243.8 trillion or $10.6 billion), Halong-Mong Cai (VND12.66 trillion or $550.43 million), Lang Son-Cao Bang (VND10.5 trillion or $456.5 million), Dau Giay-Lien Khuong (VND6.18 trillion or $268.7 million), and Bien Hoa-Vung Tau (VND14.9 trillion or $647.83 million).

Cement and clinker market in Vietnam predicted to develop in 2021

According to FiinGroup, a data provider platform, the Vietnamese cement industry expanded by 0.9 per cent in 2020, mainly driven by buoyant clinker and cement export activities while domestic sales decelerated due to the negative impact of the pandemic.

Given weakened domestic demand and the rise in fuel costs, listed cement manufacturers recorded deteriorating average earnings before interest, taxes, depreciation and amortisation (EBITDA) from 17.0 per cent in 2019 to only 15.8 per cent in 2020.

Domestic cement consumption reached 62.1 million tonnes in 2020, declining by 5.6 per cent on-year due to a negative impact of COVID-19. By region, sales in the north and the south contracted by 8.2 and 6.5 per cent, respectively, while Central Vietnam recorded a slight increase by 1.8 per cent thanks to the rebuilding and reconstruction after the heavy storms in the summer 2020 and a boost in the construction of industrial parks.

Meanwhile, clinker and cement export volume continued experiencing strong growth momentum with a surge by 14.9 per cent on-year in total export volume in 2020. The market is driven by high demand from traditional export markets including China and the Philippines as well as Vietnamese cement manufacturers’ effort to tap on new markets.

Despite a supply surplus situation, leading private cement manufacturers continue to develop new facilities aggressively amid COVID-19 to meet demand from the overseas market. Particularly, many expansion projects developed by local private groups including Vissai, Long Son, Thanh Thang, Fico-YTL, and SCC-VN are expected to launch commercial operations in the next five years, boosting Vietnam's production capacity to 149.3 million tonnes of cement per annum by 2025.

Local private manufacturers continued leading the market, accounting for 41 per cent of the market share of domestic cement sales volume in 2020. VICEM and leading private players such as Vissai and Long Son recorded a good performance with a full utilisation rate of 100 per cent in 2020 while foreign-owned players’ figure slumped to 65 per cent in 2020.

The Vietnamese cement sector witnessed a deteriorating profit margin due to the rising fuel costs and slow domestic cement consumption. Listed cement manufacturers recorded a deteriorating average EBITDA margin from 17.0 per cent in 2019 to only 15.8 per cent in 2020. This could be explained by a 6.3 per cent slump in net sales due to low demand in the domestic market and a surge by 20 per cent in coal price (which is driven by rising demand from China and reduction in the production of major suppliers such as Australia). In addition, given fierce competition due to low demand, cement manufacturers spent higher marketing and selling expense to boost sales, contributing to lower EBITDA margin for 2020.

The domestic cement market in Vietnam is forecast to have a neutral outlook in 2021 while cement and clinker export is projected for a positive outlook thanks to high demand from overseas buyers and local manufacturers to explore new markets.

|

|

|

Coolmate draws $500,000 investment from STIC Investments

Coolmate, a Vietnamese men's clothing brand selling through its own e-commerce store, has recently wrapped up a $500,000 pre-A round investment from South Korea’s STIC Investments.

Established in February 2019, the Coolmate startup specialises in selling "Made in Vietnam" apparel products directly to end-users. The startup aims to generate VND139 billion ($6 million) in revenue in 2021 after posting a revenue of VND39 billion ($1.7 million) last year.

STIC Investment is an investment fund based in Korea that manages nearly $1.4 billion in capital and has invested in more than 450 companies in Asia. STIC Investment is an early investor of Tiki, Grab, and Jo2Yoy. Prior to Coolmate, STIC has most recently poured $2 million in EcoTruck, a logistics startup.

Coolmate will use the fresh funds to develop its key areas of operation, including expanding its product portfolio to serve the demand for men's clothing and focus on materials to bring unique experiences to customers. Also, it will invest in technology to take autonomy of its sales, operation, and customer care.

Part of the fund will be invested in human resources to improve team capacity. Meanwhile, it will expand new business models such as Print-on-Demand and Subscription packages.

In 2020, Coolmate secured seed round investment from 500 Startups Vietnam.

The representative of Coolmate said that at the time of the pre-A round its revenue has exceeded last year’s results. The startup also maintains a growth rate of 15-20 per cent per month and aims to stage an initial public offering in 2025.

Ambitious railway development plan in Vietnam until 2030

Along with upgrading existing railway routes, Vietnam has ambitious plans to develop a number of new ones during the 2021-2030 period to strengthen regional economic development.

According to the draft planning on railway development until 2030 with a vision to 2050 submitted by the Vietnam Railways Administration to the Ministry of Transport (MoT), the market share of railway would be increased to 0.3 per cent in cargo transportation and 1.08 per cent in passenger transportation by 2030.

To achieve this goal, the national railway network will be extended to 16 major routes with a total length of 4,750km. The number includes seven existing routes and nine new lines.

Among the nine new routes, top priority is given to the North-South high-speed railway project, with plans to build the first two routes: Hanoi-Vinh and Nha Trang-Ho Chi Minh City.

Dang Quyet Tien, head of the Corporate Finance Agency under the Ministry of Finance, said that the North-South high-speed railway project will have big socio-economic influence, promoting the development of sectors like mechanics and high technology.

Regarding capital sources for this project, Tien said that when this project is included in the public investment programme, there will be ways to attract official development assistance (ODA) funds, and government bond issuance, and others.

Vu Anh Minh, chairman of Vietnam Railways said, "If we divide investment in the high-speed railway project into stages, I think it’s better to invest in the Hanoi-Danang and Ho Chi Minh City-Nha Trang routes first, instead of the Hanoi-Vinh segment as proposed in order to optimally meet demand. In addition, the central region is Vietnam's centre for tourism, especially Nha Trang and Danang which are attracting touritsts from both the southern and northern provinces,” the chairman explained.

In addition to the proposal to develop the first two routes on the North-South high-speed railway, the draft planning also proposes eight new lines, four of which would connect to seaports. They include the Yen Vien-Pha Lai connecting with Cai Lan seaport, and the one connecting with Lach Huyen International Gateway Port.

In the next 10 years, the draft also proposes prioritising railway routes connecting regions, including Dong Ngoc Hoi-Lac Dao-Bac Hong, Thu Thiem-Long Thanh, and Ho Chi Minh City-Can Tho, and others.

Along the new developments, the draft proposes an investment of about VND47.3 trillion ($2.05 billion) for upgrading existing railway routes until 2030 in order to increase operation efficiency.

ODA, foreign loan disbursement standing at just 7.5 pct.

Only 7.5 percent of official development assistance (ODA) and foreign loans have been disbursed since the beginning of the year according to the Ministry of Finance (MoF).

Hanoi - Only 7.5 percent of official development assistance (ODA) and foreign loans have been disbursed since the beginning of the year according to the Ministry of Finance (MoF).

This rate is too low, Deputy Minister Tran Xuan Ha told a June 11 meeting between ministries and sectors on disbursement.

He proposed that ministries, sectors, and project owners adopt more drastic measures to complete their tasks.

Truong Hung Long, director of the ministry’s Debt Management and External Finance Department, cited data from ministries and sectors in saying that, as of June 10, only 1.25 trillion VND (54.6 million USD) worth of ODA and foreign loans had been disbursed, equivalent to 7.53 percent of the assigned estimate.

Only five out of 13 ministries and sectors have disbursed public investment from ODA and foreign loans this year.

The MoF said the partial completion of investment procedures for investment projects has resulted in slow disbursement, together with the COVID-19 pandemic.

Many projects that have been allocated capital and completed investment procedures, meanwhile, have been slow in site clearance and resettlement.

To fulfil disbursement plans, Long stressed the need for synchronous and drastic measures in the entire political system, the Government, ministries, sectors, and localities.

It is necessary to review the detailed allocation of estimated capital to each project, ensure the progress and disbursement needs of each project, remove obstacles and difficulties in project implementation and disbursement, and speed up disbursement for potential projects and those that have completed investment procedures, bidding, and contract approval.

The MoF also suggested that the Ministry of Planning and Investment coordinate with relevant agencies in reviewing and evaluating public disbursement in the past, clearly identifying any difficulties and obstacles and proposing solutions to address them.

Hopes raised on divestment increase for stock synergy

Some freshly-adopted regulatory moves are expected to facilitate more advantageous prerequisites for Vietnamese state-owned enterprises to pick up their divestment pace, and thus enrich the domestic stock market with foreign capital inflows.

State Capital Investment Corporation (SCIC) has unveiled its divestment plan for 88 state-owned enterprises (SOEs) in 2021, including 31 listed companies. A big name topping the list is Saigon Beer-Alcohol-Beverage Corporation (SABECO) with a charter capital of just over $277 million, of which SCIC owns 36 per cent.

Meanwhile, FPT has a charter capital of $337.4 million, of which SCIC holds 6 per cent. Other companies include Song Da Corporation (SCIC owns 99.79 per cent) and Vietnam National Textile and Garment Group (SCIC owns 53.49 per cent), to name a few.

The lengthy divestment process has deterred investors’ appetite. SCIC has held auctions several times for 6 per cent ownership at FPT but there were no investors to participate due to complex and strict procedures. However, the shares increased to around VND95,000 ($4.10) apiece as of June 1 – a relatively high price for investors at the moment.

In another case, a sharp rise in MSB shares (nearly double the starting price that the Debt and Asset Trading Corporation applied at the end of last year) has also posed challenges for foreign financiers.

SCIC admitted not all of the sales could reap benefits, as only a few SOEs are proving lucrative to investors. As SCIC only holds a minority stake, it is impossible to have an influential impact in management if sales are executed successfully, which make such auctions less appealing to buyers.

However, the mechanism for non-voting depository receipts (NVDRs) – one of the most effective ways to entice foreign capital into Vietnam – is still stuck in the mud.

While waiting for NVDRs, foreign investors, particularly ones who wish to buy shares in listed SOEs, must purchase from another non-national at a price which will typically be 7-15 per cent above the prevailing listed price, according to VinaCapital’s calculation.

This dilemma also exacerbates roadblocks for international funds to expand their footprint in Vietnam, thus hampering state capital divestment pace. In a broader context, lack of foreign ownership easing conditions also thwarts Vietnam’s equity market to be upgraded to emerging status.

Le Song Lai, deputy general director of SCIC, said that long-awaiting guidance for Decree No.140/2020/ND-CP issued last November on changes to the legal framework covering the divestment of SOE capital in private enterprises have paralysed SCIC’s divestment activities since the beginning of this year.

Thus far, the regulatory obstacles have seriously hampered state divestment, making it lag behind stock market growth momentum.

Seck Yee Chung, partner at Baker McKenzie Vietnam, told VIR that it is interesting and encouraging to see SCIC announce its plan to divest from the 88 companies. It continues the government’s long-standing agenda to reduce state holdings in a whole raft of originally state-owned and presently equitised companies.

In this regard, peak excitement was last reached in 2017 with ThaiBev’s majority stake acquisition in SABECO. Since then, no divestment has generated the same amount of attention and eye-catching deal size, simply because no similarly-sized companies have been put up for investors since. In the meantime the government, various stakeholders, and investors at large continue to monitor the outcomes and developments of the landmark deal.

With the onset of the pandemic in early 2020 came new uncertainty in the market but SCIC maintained its divestment plans for the year. In parallel, various equitised companies also had their state holding transferred to SCIC – including SABECO, where the state holding was originally by way of ownership of the Ministry of Industry and Trade.

“Again, these are indications that the government is staying the course on state divestments, even while recognising and addressing the challenges,” Chung added. “The companies in the new 2021 list are diverse in terms of size and sector. It has some very well-known names, like SABECO, FPT, and Bao Viet Group. However, there are also many companies that have considerably smaller book sizes. At this point, whilst this news will generate interest, it is too early to tell to what extent there will be landmarks deals created.”

According to the latest report by the Finance and Budget Committee sent to the National Assembly Standing Committee, only 27.3 per cent of the divestment plan in 2020 was fulfilled with 89 SOEs yet to be equitised as of last December. The coordination between the owner’s representative agency and local authorities on disposition of public property remained sluggish.

The committee proposed the government to accelerate the process of divestment, equitisation of state capital, and rearrangement of SOEs in production and business fields where non-state economic sectors operate more efficiently.

On May 26, the prime minister issued Circular No.36/2021/TT-BTC on guiding a number of contents on state capital investment, management and use of capital and assets at SOEs as prescribed in various decrees over the past five years.

Circular 36 guides many provisions, of which the most important one is the guidance on determining enterprise value based on their cultural and historical values.

Circular 36 is expected to take effect from July 10 this year. Thus, SCIC can start execute some divestment deals, the corporation said.

Thus, investors can lay their hopes on an accelerating divestment pace in the second half of this year, which is a main catalyst to boosting the domestic stock market’s synergy.

In the same vein, analysts at Mirae Asset Securities said that following the successful earnings season, the domestic stock market is expected to extend its further rise within the range of 1,130-1,480 points, with the base-case target of 1,300 points.

“Among them, one of the market’s main drivers is SOE privatisation and a wave of bank initial public offerings or transfers to the main bourse. Other factors include the government’s commitment to controlling the pandemic, the rollout of vaccinations, buoyant market liquidity, accelerated credit growth combined with low interest rates, and others,” Mirae Asset Securities highlighted.

In order to create significant investor interest and larger-sized deals, Chung from Baker McKenzie believed that the company would need to be a market leader and a sizable business to begin with. Meanwhile, the state would also need to be prepared to divest a majority stake so as to essentially give the new investor at least simple majority control. This also means that investors will be looking out to see if there any foreign ownership caps for these companies.

In terms of legal framework, Vietnam has new investment, enterprise, and securities laws that took effect in January, as well as a more robust merger control regime that took effect from around mid-2020. This means that state divestments in 2021 will put to test these new laws, regulations, and procedures, according to Chung.

On the upside, he said that there is more leeway under the new laws under which foreign ownership may go above the 49 per cent cap that was imposed on all public companies under previous laws. In addition, there is no longer a legal requirement for a shareholder to hold shares for at least six months before being allowed to nominate a board of management member.

“However, the merger control rules are much more encompassing and it is likely that any majority acquisition, and the parties and company involved, will meet the notification thresholds and will trigger merger filing. The preparation, application, and review process can be time-consuming - especially if the target is a market leader,” he added.

In 2021, the divestment of SOEs is expected to generate around $1.73 billion. Dang Quyet Tien, director of the Corporate Finance Department under the Ministry of Finance, said that the implementation of state divestment and equitisation this year depends on the control of the pandemic. If it continues to cause major disruption, it will be difficult to organise the bidding auction for divestment. On the other hand, the result of divestment depends on movements in the stock market.

“Hopefully in the second half of this year, the progress of state divestment and equitisation will pick up thanks to a more open valuation of enterprises, attaching responsibility to the valuation organisation. Besides that, the auction regulation is more in line with the market mechanism, making auction activities more attractive to investors,” he added.

Energy mix for Vietnam with LNG-to-power

Supported by the favourable geographical and natural conditions and constrained by the restrictions on thermal power projects in the last few years, Vietnam has been promoting the concept of using liquefied natural gas for power production. Vaibhav Saxena and Tu Hue Anh from Vilaf law firm delve into the opportunities and key obstacles under the new rules.

Guided by Politburo’s Resolution No.55/2020-NQ/TW, the recent draft decision of the Prime Minister to approve the draft Power Development Plan VIII (PDP8) specifies 45 major liquefied natural gas (LNG) projects with total capacity of just over 53,000MW, lining up in the list of power ventures which are of national importance and a development priority from now until 2045.

The LNG infrastructure is strongly promoted under PDP8, setting a steady foundation for the growth of such projects and its related businesses in Vietnam.

Under Vietnamese laws, a LNG project can be developed in either a public-private partnership (PPP) initiative whereby the investors will cooperate with the state to develop and operate it through signing and performing the PPP contracts; or an independent power producer (IPP) project whereby investors will wholly develop it by themselves.

For an LNG project to be considered under the PPP form of investment, the total capital must be not less than VND1.5 trillion (approx. $65 million). However, the capital requirements for certain ventures in practice, particularly involving foreign inventors, can be substantially higher, normally around $2.5-3 billion in the past, and now perhaps $5 billion or higher for large-scale LNG projects.

Investors of a PPP scheme shall have to sign a PPP contract with the state agency in order to implement the project. Types of PPP project contracts under the Law on PPP are as follows (see red image):

The model contracts for each type of PPP project shall be further specified by the government.

Generally, basic steps for implementation of a LNG venture in PPP form shall be as follows (see pink image):

The time period for the investor to be officially selected as the developer of the PPP project will be substantially long due to the heavy involvement of the government and the sophisticated requirements under the bidding procedures. In return, the investor will be entitled to better governmental support and guarantee (e.g., guarantee on foreign currency convertibility) which are required to raise project finance from foreign lenders.

The funding and development of an IPP LNG project shall mainly be governed by the Law on Investment and its implementing regulations as well as Circular No.57/2020/TT-BCT.

- There are four general policies – on power purchaser, electricity generation price, a power purchase agreement (PPA), and construction of transmission lines and substations.

At present, Electricity of Vietnam (EVN) and its subsidiaries are no longer the sole wholesale power purchaser from LNG power generators/sellers. Circular 57 has allowed big power consumers and wholesale power purchasers to purchase power from the power seller, which aligns with Vietnam’s plan to develop a fully competitive power market.

If EVN or its subsidiaries is a contracting party to the PPA, based on the model PPA provided under Circular 57, the investor of the LNG project as the Power Seller, and EVN or its subsidiaries as the power purchaser, can negotiate, agree, and supplement certain terms which are suitable for the actual conditions of the specific venture if necessary. This regulation may suggest that parties can have more flexibility in negotiating upon the technical clauses under the PPA.

Under Circular 57, such projects are not entitled to enjoy the feed-in tariff mechanism. Rather, it provides the basic principle to determine the electricity generation price for LNG initiatives.

This generation price is the aggregate of the power purchase agreement price and the specific connection price, which shall be agreed upon by the parties and determined by the method as specified under Circular 57.

The specific connection price is a new component introduced under Circular 57, which is for the LNG project to recover from the grid connection costs incurred by or allocated to the investor to build the transmission lines and the power substation(s) from the distribution yard of the power plant to the main grid connection point as agreed with the power purchaser; or assigned by the competent state authority.

Under Circular 57, the competent state authority can assign the power seller to establish a separate project to build the transmission lines and the power substation to load electricity from their power plant to the main grid connection point. However, we have to wait for further guiding implementations to see how this mechanism will be implemented in practice.

However, the circular regards the construction of transmission lines and power substation as the power seller’s obligations, which may cause additional liabilities to the investor. Thus, they should seek consultation with the power purchaser and local authorities upon this obligation, especially taking into account its financial/technical capacity.

- Investment procedures

The investor can fund an IPP LNG project through two options: registering for investment of a greenfield LNG scheme and setting up an economic organisation as the project company to implement it in Vietnam; or brownfield – putting money into an existing project by way of acquiring existing shares or subscribing for new shares in the relevant Project Company.

If following option 1, there are four key steps. First, the selection procedure is applied in the circumstances and methods as stipulated under the Law on Investment, which will take a substantial amount of time due to the complex bidding/auction procedures.

Second is in-principle approval. Depending on the nature and scale of the project, it can be subjected to the approval authority of either, the National Assembly of Vietnam, the Prime Minister, or the provincial People’s Committee.

After that step, the competent provincial Department of Planning and Investment (DPI) will issue the investment registration certificate to formalise the registration of the LNG project.

The next step is the enterprise registration certificate for the project company. The investor must set up a project company in Vietnam to start implementing the LNG scheme.

If a foreign investor and following option 2, they must register for the approval of the acquisition or subscription of the existing shares/new shares in the Target Company with the competent DPI, which is required in the following three cases:

First, if the acquisition or subscription increases the ownership ratio of the foreign investor(s) in the Target Company which conducts business in areas with certain market access conditions applicable to foreign investors.

Second, if the acquisition or subscription results in foreign investor(s) holding over 50 per cent of the charter capital of the Target Company in the following cases: charter capital ownership ratio by the foreign investor(s) is increased from less than or equal to 50 per cent to over that amount; or charter capital ownership by them is increased while such foreign investor is holding over 50 per cent of the charter capital of the Target Company.

Third, if the foreign investor acquires or subscribes to shares of the Target Company which has a land use right certificate for land on an island or in a border commune; in a coastal commune; or in another area that affects national defense and security.

The first major barrier currently is a lack of an exhaustive legal framework and implementing regulations. Given that the Vietnamese LNG market and its legal framework are still at an early stage of development, the investment and implementation of such projects and especially LNG-related businesses are expected to face uncertainties and ambiguities. For now, Decree No. 87/2018/ND-CP is acting as the key piece of legislation governing the trading, importing and transporting of LNG. However, the conditions therein are quite general and ambiguous, which may cause confusion for investors.

Second is the lengthy regulatory approval process for the full project chain. The LNG market is relatively new in the country and Vietnam still lacks supporting infrastructure. Thus, investors participating in the sector may need to fund all aspects of the LNG venture chain and to ensure smooth operation of their projects, which shall involve complex and lengthy regulatory approval processes associated with each component of the LNG-to-power chain.

The third issue involves foreign currency availability. Like other countries, Vietnam’s foreign exchange reserves are limited and there exists a risk that the availability of US dollars in the country may be rationed at times, which poses a challenge for any investors who want to convert VND into USD to conduct their business.

Finally, the Law on Land allows investors to mortgage both their land use rights as well as assets attached to land (understood as immovable assets) as collateral(s) to raise financing from local banks in Vietnam. However, the land use rights can only be mortgaged where the land rent due to the state authorities has been paid in a one-off payment. This means that, if the project land is exempted from the land rent (as an investment incentive) or the land rent is paid on an annual basis, the land cannot be used as a security for raising finance to support the LNG project.

Source: VNA/VNS/VOV/VIR/SGT/Nhan Dan/Hanoitimes